Balancing Treasury Market Stability and Systemic Risk

April 21, 2025 By Sage Advisory

In an interview last week Treasury Secretary Scott Bessent, who has been vocal about his desire to lower the 10-year rate, mentioned what he sees as the Treasury’s toolkit for doing so. One of those measures was the lowering of the supplementary leverage ratio (SLR) for banks, which he described as something that will “allow banks to buy more Treasuries without a big capital charge . . . I expect we will have created a new buyer for Treasury securities.”

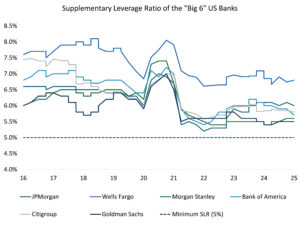

The SLR is a binding capital requirement intended to limit excessive balance sheet expansion among large banking institutions. It was introduced as part of the Basel III post-crisis regulatory reforms and implemented in the US beginning in 2014. Unlike risk-weighted capital ratios, which adjust capital requirements based on asset riskiness, the SLR applies uniformly across asset types — treating US Treasuries, reserves, and loans equally, with the goal being to limit banks’ balance sheets from growing too large and limiting systemic risk in a crisis. For US global systemically important banks (GSIBs), the minimum SLR requirement is 5%, meaning they must hold 5% of common equity capital relative to their total leverage exposure. The largest US banks typically maintain an SLR well above the required level, although SLRs have trended lower toward the 5% minimum in recent years.

Source: Sage, Bloomberg

In response to the significant balance sheet expansion driven by monetary and fiscal interventions, the Federal Reserve announced in April 2020 a temporary exclusion of US Treasury securities from the SLR denominator for bank holding companies. This action was intended to mitigate binding capital constraints arising from a rapid influx of low-risk assets, particularly as banks absorbed deposits and acted as intermediaries in strained Treasury markets.

The exclusion expired in March 2021. Although regulatory agencies indicated they would review the long-term calibration of the SLR, no structural changes have been implemented.

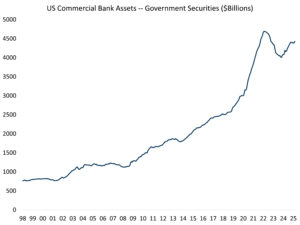

The mechanics of the SLR have direct implications for Treasury market functioning. When Treasuries and reserves are included in the leverage exposure measure, increases in these positions consume balance sheet capacity. As a result, banks may be disincentivized from engaging in market-making or absorbing large Treasury flows, particularly during periods of supply shocks or liquidity stress, especially as the banking sector’s holdings of Treasuries have grown significantly in recent years.

Source: Federal Reserve

A reintroduction of SLR relief, either through a renewed exemption of Treasuries and reserves or as a recalibration of the leverage exposure definition, would likely produce several market effects:

- Banks would have greater capacity to hold US government securities, potentially reducing auction tail risk and compressing term premia.

- Market liquidity would improve. Reduced balance sheet frictions would enable more active market-making and better absorption of issuance. Also, banks would be more willing to provide financing in the repo market against Treasury collateral, reducing the likelihood of funding stress in short-term markets.

The main trade-off from the loosening of regulatory burden for Treasuries would be its potential negative effect on the broader objective of systemic resilience. The SLR was designed to provide a capital floor regardless of portfolio composition. Minimizing this requirement could risk reintroducing moral hazard, particularly in a financial system where perceived safe assets dominate balance sheets. A regulatory decision to relax the SLR would create more capacity for Treasury purchases, but they do not necessarily compel banks to buy Treasuries. Additionally, the Federal Reserve would have to loosen this requirement, which may prolong the process as it requires Treasury/Fed coordination.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.